When you were a kid, did you ever dream of growing up to be someone’s cashier? Maybe not.

But whenever you buy shares in a company’s IPO, that’s exactly what you become. Whether being an early liquidity investor is good or bad is hard to say in the short term. In the long run, you will certainly find out.

The main reason I have invested a greater percentage of my capital in private companies over the past 20 years is because private companies are staying private longer. More of the profits are being accrued to private investors at the expense of future public investors.

SpaceX, for example, was founded on March 14, 2002. It will finally go IPO 24 years later, on June 12, 2026. Microsoft was private for 11 years, Google for 6 years, and Facebook for 8 years before going public. Those who bought their IPOs and held onto them have done well. I’m not sure the same will happen with SpaceX.

So, one of the most common questions I get newsletter readers The latest is: Will you invest in SpaceX’s IPO?

My answer is NO, for several reasons.

I don’t want to run out of liquidity for big IPOs

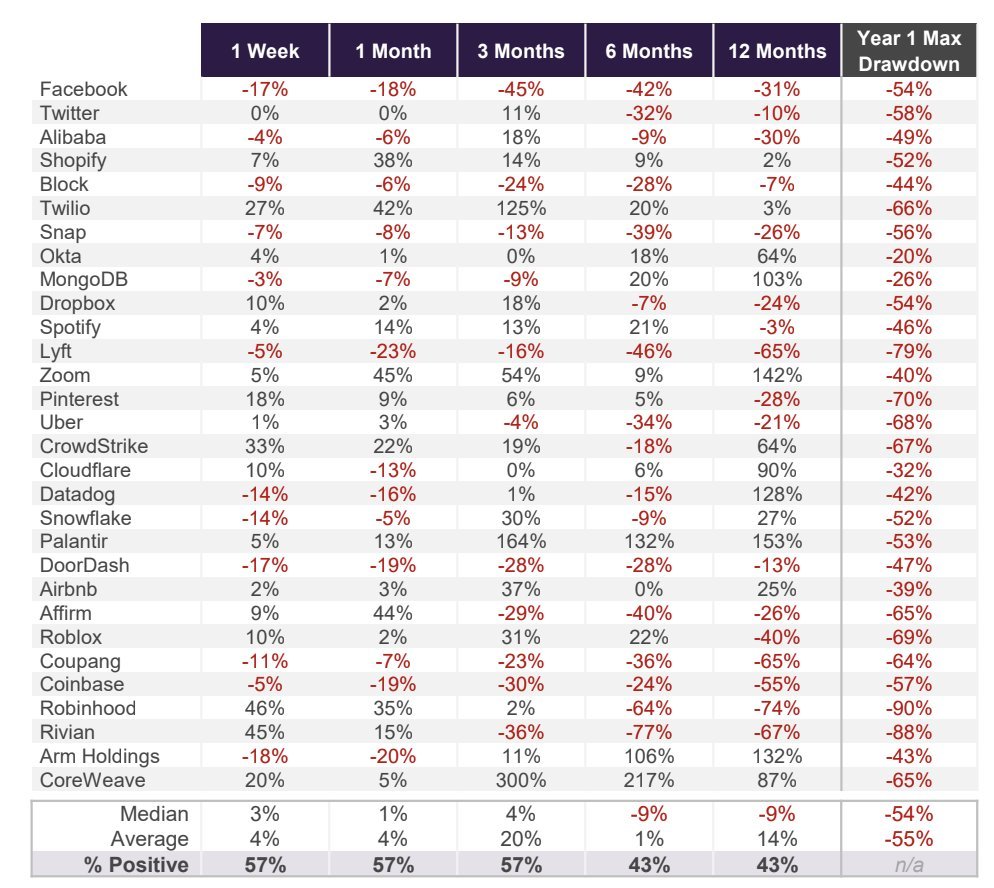

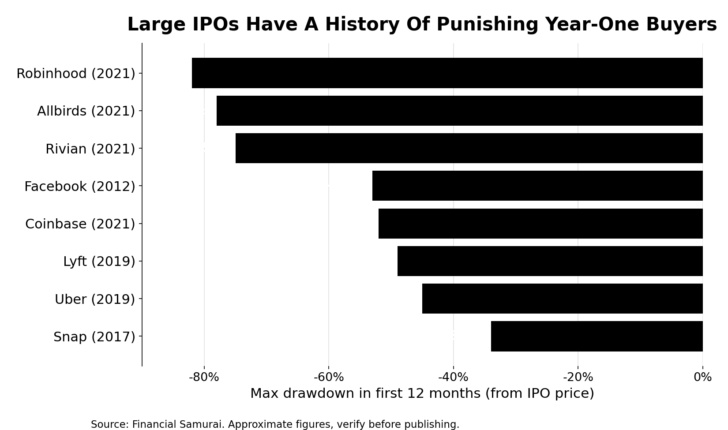

History is not kind to large ($1+ billion) IPOs. Take a look at this chart that highlights the share price performance of selected large IPOs by time period after listing. Note the final column, Year 1 Max Drawdown.

History is not on the side of the big IPO investors, and that’s what happens if you buy shares at the IPO price.

The downside gets worse if you buy a big IPO that goes down and then follow it. A recent example is the IPO of Figma (FIG) on July 31, 2025 at $33 per share. It increased and reached a value of about 122 dollars. Today the share price is around $22. This is approximate.

I don’t want to be part of the retail frenzy

Morgan Stanley valued Figma’s stock appropriately for that time. Retail strength was the main reason the share price rose on the first day.

I have been investing in public stocks since 1996 and have helped over 100 companies IPO during my days at Goldman Sachs and Credit Suisse. My experience is simple. Greater retail participation creates more volatility because retail investors are classic paper hands and short-term holders.

So with SpaceX raising $75 billion, the largest IPO in history, and allocating 30% of the deal to retail, roughly $22.5 billion in equity, I see this as a net negative, not a net positive.

Volatility will be wild. If you are participating in the IPO, it is best to watch your position carefully on the first day and first week. Maybe take the day off to be one manic day traderone of the worst things you can do for your investments.

I don’t want to run out of liquidity with wild valuations

At SpaceX’s ( SPCX ) target price of $135 a share, valuing the company at about $1.77 trillion, its price-to-sales ratio will be more than 90-to-1. I think this is the highest P/S ratio in the history of IPOs. Even IPOs that went public at half the multiple continued to underperform the market over the following three years.

Do you really want to run out of liquidity for a company that trades at such an extreme valuation when the S&P 500 is also at elevated levels? I don’t.

Here’s a look back at all the companies that traded over 10 times sales at the dot-com peak and what happened next.

- Cisco: ~25x sales, P/E over 200. Down -90%. It finally broke the 2000 high in December 2025, 25 years and 8 months later.

- Intel: ~13 times sales. Decrease -82%. It finally broke the 2000 peak in May 2026, almost exactly 26 years later.

- Microsoft: ~25x sales. Decrease -65%. It took 16 years and 8 months to reach a new level (October 2016).

- Qualcomm: ~30x sales. Decrease -88%. It took roughly 20 years to break down.

- Sun Microsystems: ~10x sales. Fall -97%. Acquired by Oracle in 2009.

- JDSU: ~50x sales. Drop -99%. Stripped to pieces.

- Yahoo: ~50x sales. Fall -97%. I didn’t want to sell to Microsoft for $44 billion, and eventually sold to Verizon for a tenth of that.

- Nortel: ~15x sales. Bankrupt in 2009.

- Amazon: ~30x sales at peak. Fall -97%. Definitely a big winner now, but not before a lot of pain.

Investing in reasonable valuations matters. Buying at nosebleed IPO levels is the ultimate fool theory in action, especially when the company is not profitable. I had a front row seat The craze of 1999 sitting on the sales / trading floor of GS at 1 New York Plaza. Many investors lost their shirts within a year.

The best move is to wait for the buzz to die down, then buy if you believe in the business and its growth trajectory. Retail has a fantastic way of offering hot IPOs to irresponsible levels, only to have the price correct once management reports the first two quarters.

Anyway, you’re going to own SpaceX, so why pursue it?

Here’s the kicker. With a valuation of $1.77 trillion, SpaceX debuts as one of the top 10 American companies. Index funds will be forced to buy it, which means you will be forced to buy it too, automatically, through S&P 500 and total market funds.

You don’t need to follow the IPO to own SpaceX. Wait a few quarters and the market gives you a position at whatever the real clearing price turns out to be. Let the index do the work.

And remember, most retail investors aren’t going to buy IPO stock at $135 anyway. You will get a small partitionif there is.

To almost everyone, “buying the SpaceX IPO” really means buying SPCX at the opening on the first morning, after it has already gone up (or down). This is not the IPO purchase. This is volunteering to be the outgoing liquidity.

Already own shares in SpaceX through venture capital

Finally, I don’t want to be the exit liquidity for SpaceX because I already own funds that will likely sell some or all of their holdings of SpaceX in the IPO or after the lockup expires.

A traditional venture capital growth fund I invested in in 2022 had about 10% of its fund in SpaceX as of 1Q2026. I expect they will eventually sell all the property because they are required to return capital to the LPs.

I also own a significant amount of Fundrise Innovation Fund, VCX, which had a position of about 5% of SpaceX as of 1Q2026. VCX is not required to sell anything that goes public, as it is a perpetual equity fund.

However, I have a large enough position in SpaceX that buying more would not be prudent on a risk/reward basis and asset allocation perspective. And even if I didn’t own any of them through venture funds, I still wouldn’t buy the IPO for the above reasons.

What I would actually do instead

To be fair, here is the buying case. Starlink is a real cash flow machine now, Starship can open up a whole new market and there is no comparable competitor. If you believe SpaceX becomes the AWS of space, $135 might seem cheap in ten years.

I’m not saying SpaceX is a bad company. I’m saying I don’t want to pay any price for a big company. Price is what protects you when the story gets in the way.

So what would I do? I would wait. Let the lockdown expire, let the first earnings reports land, let the frenzy burn. If the business is as good as the bulls say, it’s still as great at $110 as it is at $135. And if it isn’t, I’ll be happy to let someone else find out first.

If you simply must own stocks, then buy with your spare cash that you can 100% afford to lose.

But as a long time Tesla shareholder, I hope SpaceX buys Tesla at a 50% premium!

Questions and suggestions for readers

Readersare you okay with exiting liquidity for a hot and expensive IPO? What is your strategy for buying IPOs? Are you buying the SpaceX IPO and why? What price do you think it will trade at after the first day? And do you think these mega IPOs will siphon liquidity from the public markets and trigger a correction?

If you want to build more wealth than 94% of the American population, pick up a copy of my USA Today national bestseller, Millionaire Points: Simple Steps to Seven Figures. Life is much easier when you have more money.

If you want to achieve financial freedom faster, subscribe to my site free weekly newsletter and join over 60,000 readers. I launched Financial Samurai in 2009, and it has grown into one of the largest independently owned personal finance sites today. Everything is written based on first-hand experience, because money is too important to leave to the pontificate.