Investment professionals have long relied on factor investing — strategies built around characteristics such as value, momentum and quality — to generate returns beyond the broad market. But predicting which factors will perform well in the future has remained challenging. Liyao Wang and Ming Zeng, authors of the December 2025 study “MAX Factor and Predictable Factor Returns”, introduced an intriguing predictor: the MAX factor, which captures extreme daily gains within a month.

What Researchers Examined

Research findings (see for example here AND here) have found that extreme returns are found to be a useful source of information at the individual stock level. The MAX factor study investigated whether the maximum daily return experienced by a factor in a month contains valuable information about the future performance of that factor. Unlike traditional predictors such as factor momentum (which looks at cumulative performance over recent periods), the MAX factor isolates a single data point: the highest daily return a factor achieves in a given month.

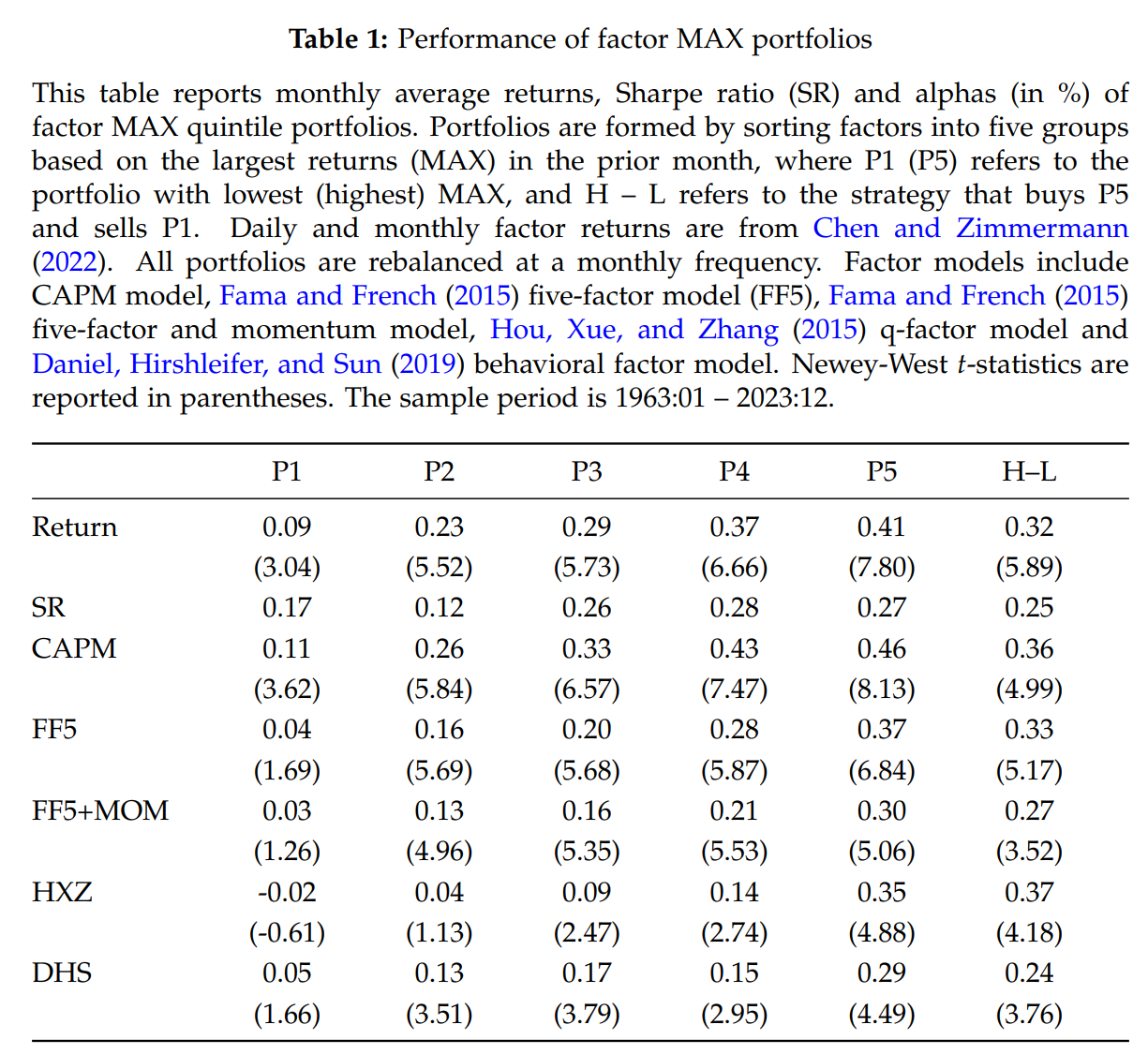

The researchers analyzed 172 equity factors from 1963 to 2023, ranking them each month into quintiles based on the previous month’s maximum daily return. They then tracked how these portfolios performed in the following month.

Key findings

1. Strong return predictability

Factors with higher maximum daily returns significantly outperformed those with lower maximum returns. The strategy of buying factors with high MAX and selling factors with low MAX is created:

- 0.32% per month in raw returns (with a t-statistic of 5.9) – the average monthly returns of the MAX factor portfolios increased from 0.09% for quintile 1 to 0.41% for quintile 5.

- Statistically significant risk-adjusted returns ranging from 0.24% (the behavioral model of Daniel, Hirshleifer, and Sun) to 0.37% per month (model with factor q Hou, Xue, and Zhang) depending on which of the five factor models were used (the other models used were the CAPM and the five– and with six factors Fame and French models).

- Over the full sample period, this translated into cumulative alpha of $9.58 per dollar invested.

- Limited pullbacks, suggesting that MAX factor returns are not concentrated in a few specific historical periods.

2. Distinct from the moment of the factor

While the MAX factor is related to factor momentum (since extreme returns often coincide with strong average performance), it captures different information. The MAX factor strategy continued to generate significant abnormal returns even after controlling for the time series and cross factor moments.

3. It is not driven by stock-level lottery effects

The researchers ruled out the possibility that the MAX factor simply repackages stock-level anomalies associated with extreme returns or “lottery-like” characteristics. The factor-level effect remained robust after controlling for seven different stock-level anomalies, including maximum returns, individual volatility, and return distortion.

4. The power of investor attention

The study provides compelling evidence that limited investor attention drives the MAX factor effect through underreaction to factor-level news. The strategy turned out to be more profitable when:

- Factors received low investor attention – 0.42% monthly return (t-stat of 2.93) versus statistically insignificant returns for factors with high attention

- The extreme return day did not coincide with prominent macroeconomic announcements or earnings releases

- The factors were more systematic – closer to broad risk, non-diversifiable and appeared broadly across securities, asset classes and timing.

5. A tale of two MAXes

Perhaps most intriguing is that investors seem to react differently to extreme returns at different levels:

- MAX at stock level: Investors overreact, leading to subsequent returns (consistent with lottery-seeking behavior)

- MAX at factor level: Investors react less, leading to consistently positive returns

This asymmetry explains why MAX stocks negatively predict stock returns while MAX factor positively predicts factor returns.

6. A counter-moment split at MAX

At the individual stock level, original anomaly MAX documented by Turan Bali and co-authors is an opposite signal: lottery-like stocks with very high daily maximum returns in the past tend to perform poorly then, so the profitable trade is effectively long low-MAX, short high-MAX. In contrast, the MAX factor is used as a momentum-style signal in the factor space: factors that experience an extreme positive daily return within a month tend, on average, to they continue outperforming in the next month, just like a time-series-momentum factor strategy.

This “aggregation-level shift” echoes a broader pattern in the literature: single-stock returns often exhibit short-term returns (STREV-type effects), while diversified factor returns exhibit positive autocorrelation that supports factor momentum and MAX-type continuation bets. For practitioners, the key is to recognize that a characteristic that is inverse in the stock cross section can be legitimately traded as a momentum signal once it is embedded in a factor and treated as a time series.

Results are hypothetical results and are NOT an indication of future results and do NOT represent returns actually achieved by any investor. Indices are not managed and do not reflect management or trading fees, and one cannot invest directly in an index.

Key Investor Relations

1. Monitor extreme factor returns

Investors should pay attention not only to the average performance of factors, but also to extreme daily performances. A factor that experiences extremely high daily returns can signal continued performance in the month ahead.

2. Combine with existing strategies

The MAX factor complements rather than replaces current factor strategies. Investors can potentially increase returns by incorporating both signals into their factor timing decisions.

3. Focus on low-attention environments

The effect of the MAX factor is stronger when the investor’s attention is limited. Consider highlighting this signal for:

- Factors that receive less market attention

- Periods without major macroeconomic announcements

- Factors whose constituents do not declare earnings

4. Systemic factors are more important

The predictive power of the MAX factor is focused on more systematic factors (those that explain the widest market variation). This suggests that the strategy works best when applied to well-defined, fluid factors rather than specific anomalies.

5. Strong in all specifications

The effect is remarkably consistent across different portfolio construction methods (such as quintiles, quartiles, or terciles), definitions (such as redefining the signal as MAX5—the sum of the five largest daily returns within a month), time periods, and factor universes. This consistency suggests that it is not a true model of market-derived data.

Implementation considerations

While the academic evidence is compelling, practical application requires consideration of:

- Transaction costs: Monthly rebalancing of many factors can be expensive

- Selection of the universe of factors: Focusing on more fluid and systemic factors can improve real-world performance

- Combination strategies: Integrating the MAX factor with momentum and other signals can optimize risk-adjusted returns

CONCLUSION

Factor MAX represents an innovative approach to predicting factor returns by focusing on extreme intra-month performance rather than cumulative returns. Evidence suggests that investors systematically underreact to factor-level news involved in these extreme returns, creating exploitable return predictability. For sophisticated investors engaged in factor investing, incorporating MAX factor signals—especially during low-attention environments and for systematic factors—can provide significant opportunities to improve performance.

The finding that investors process stock-level and factor-level extreme returns differently also provides valuable insight into market psychology and the limits of investor attention in processing complex, portfolio-level information.

Larry Swedroe is the author or co-author of 18 books on investing, including his latest, Enrich your future: the keys to a successful investment. This article is for informational and educational purposes only and should not be construed as specific investment, accounting, legal or tax advice.

–

Important discoveries

For informational and educational purposes only and should not be construed as specific investment, accounting, legal or tax advice. Some information is considered reliable, but its accuracy and completeness cannot be guaranteed. Third party information may become out of date or be replaced without notice. Neither the Securities and Exchange Commission (SEC) nor any other federal or state agency has approved, determined the accuracy, or confirmed the adequacy of this article.

The views and opinions expressed herein are those of the author and do not necessarily reflect the views of Alpha Architect, its affiliates, or its employees. Our full disclosures are available here. Definitions of common statistics used in our analysis are available here (in the last direction).

Join thousands of other readers and subscribe to our blog.