Selecting mutual funds is one of the most important tasks that investors face. However, the tool everyone is aiming for, the Sharpe ratio, tacitly assumes something most real people don’t: the ability and willingness to borrow at the risk-free rate to raise or lower the “best” fund to their preferred level of risk. Once borrowing is actually constrained, the Sharpe ratio can stop along with what investors really care about: utility. This paper argues that in this finite world, the geometric mean is a better compass. And a shrinkage-adjusted version, the generalized geometric mean (GGM), can improve real-world fund ranking and selection.

Mutual fund selection when borrowing is constrained: on the virtues of the generalized geometric mean

- Moshe Levy

- Financial Analyst Magazine, 2025

- A version of this paper can be found here here

- Want to read our summaries of academic finance papers? Check out our Academic Research Overview CATEGORY

Key academic insights

The Sharpe ratio is “almost perfect” only in a world of borrowing

With unlimited borrowing at the risk-free rate, the higher Sharpe fund can be used to match the risk of any other fund while delivering a higher expected return. This makes the Sharpe ranking extremely close to investor welfare. But this extension relies on the availability and use of leverage.

Borrowing restrictions break the Sharpe ratio welfare ranking

When investors cannot borrow, they cannot use the underlying Sharpe fund to achieve the desired risk score. In this environment, two funds with similar Sharp reports can offer very different “opportunity sets” since you only allow lending, not borrowing. This is why the Sharpe ratio can rank a fund high even when it delivers equivalent results with lower certainty for many investors.

Tthe geometric mean becomes a better practical ranking statistic

The main claim of the paper is that when borrowing is constrained, the geometric mean (GM) ranking matches investor welfare much more closely than the Sharpe ranking or the usual alpha measures. The intuition is that GM naturally rewards higher compound growth and penalizes volatility in a way that better matches limited choice.

The generalized geometric mean fixes the “estimate reality” problem.

Even if GM is the right target, estimating future GM from past returns is noisy. The proposed solution is a generalized geometric mean (GGM.) The gross, pre-fee, GM shrinks toward the sectional mean because past performance is an error-prone estimate of the future. Then deduct the fees without shrinking them, because the fees are widely known. This approach, which effectively overweights fees relative to noisy past performance, is enhanced by sample fund selection.

Practical applications for investment advisors

Use the right metric for the constraint your customer faces

Most clients do not borrow to use mutual funds. Some cannot. Some won’t. Some are effectively limited by platform rules, risk controls or common sense. Sharpe is the appropriate ranking rule only when customers can use the risk-free rate. When leverage is limited, Sharpe can misclassify funds because you cannot scale the max-Sharpe fund to the desired risk level. A GM or GGM style listing is designed for the no-loan reality, so it better matches what the customer can actually implement.

Make the fees more important because they are the part you can actually know

People often overweight recent returns and underweight fees. But returns are noisy and hard to predict, while fees are one of the few things you can be fairly certain about. GGM builds this into the ranking: it discounts past performance for estimation error, but takes fees at face value. This automatically gives the fees more influence on the decision than a naive performance screen. If your client can’t explain why a higher fee is worth it in terms of a repeatable advantage, the default assumption should be that the fee is real and the advantage uncertain.

Improve fund shortlists without pretending you can predict perfectly

You don’t need to turn your process into a math competition. Hands-on is a process improvement. When creating a shortlist, prefer measures that are consistent with limited implementation and robust to estimation errors. In practice, this means de-emphasizing Sharpe and conventional alpha screens as primary ranking tools in limited accounts and relying more on a combination of conscious metrics plus fee discipline.

Customer fit trumps metric purity

The point is not “everyone should buy GM’s flagship fund”. The point is: if you are ranking and choosing between active funds, the criteria must match the client’s set of constraints and behavioral reality.

Use retirement conversations to reset the standard

Many clients judge success by raw returns. The paper shows that raw returns can look good while risk-adjusted performance deteriorates. Advisors can educate clients to focus on the results that matter: meeting spending goals, managing downside risk, controlling taxes and fees, and maintaining a strong distribution.

How to explain this to customers

“The Sharpe ratio works best in a world where you can borrow to grow a good fund and borrow to raise it. Most people don’t invest that way. If you can’t borrow, two funds that look ‘equally good’ by Sharpe may actually lead to different results. This study suggests we should pay more attention to compound growth and fees. Fees are not sure what performance you can use. true. do on your account.”

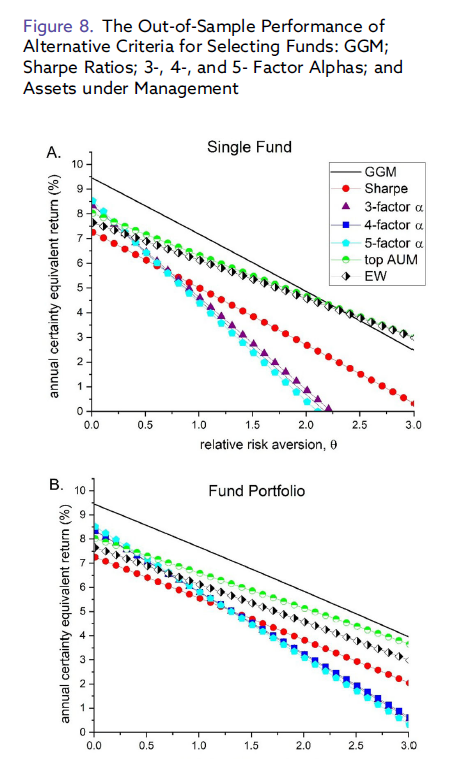

The most important chart from the paper

Results are hypothetical results and are NOT an indication of future results and do NOT represent returns actually achieved by any investor. Indices are not managed and do not reflect management or trading fees, and one cannot invest directly in an index.

ABSTRACT

The Sharpe ratio is almost perfectly consistent with investor welfare when borrowing is unlimited. However, when borrowing is actually constrained, this spread breaks down dramatically. We show that the geometric mean (GM) provides a much better alternative for ranking funds in this case. Ex-ante GM estimates can be improved by first reducing the gross sample GM and then subtracting the charges. Generalized GM (GGM) captures this idea and provides a good estimate of future net GM. We argue that mutual fund selection can be significantly improved by using the GGM instead of the more popular Sharpe ratio or alpha.

–

Important discoveries

For informational and educational purposes only and should not be construed as specific investment, accounting, legal or tax advice. Some information is considered reliable, but its accuracy and completeness cannot be guaranteed. Third party information may become out of date or be replaced without notice. Neither the Securities and Exchange Commission (SEC) nor any other federal or state agency has approved, determined the accuracy, or confirmed the adequacy of this article.

The views and opinions expressed herein are those of the author and do not necessarily reflect the views of Alpha Architect, its affiliates, or its employees. Our full disclosures are available here. Definitions of common statistics used in our analysis are available here (in the last direction).

Join thousands of other readers and subscribe to our blog.