Traditionally, balanced portfolios rely on equity and bond risk premiums to generate returns. The canonical 60% equity/40% bond allocation has produced strong long-term results, but its short- and medium-term track record includes major drawdowns. These pullbacks matter not only behaviorally, but also mechanistically, through volatility drag: large losses require disproportionately large gains to recover. This paper asks a practical question with an extremely strong empirical structure: which defense strategies have actually worked, and do the conclusions survive when we evaluate them over many centuries rather than decades?

The best defensive strategies: Two centuries of evidence

- Baltussen, Martens and van der Linden

- Financial Analyst Journal, 2026

- A version of this paper can be found here here

- Want to read our summaries of academic finance papers? Check out our Academic Research Overview CATEGORY

Key academic insights

Two centuries change the leaderboard

Most estimates of hedging strategies are limited by post-1980 data, which contain only a limited number of severe withdrawals. The authors extend the testing window to 1800 using a deep historical knitted data set with monthly frequency. This materially increases the number of significant withdrawal episodes and reduces the risk that terminations will be driven by a small set of modern crises.

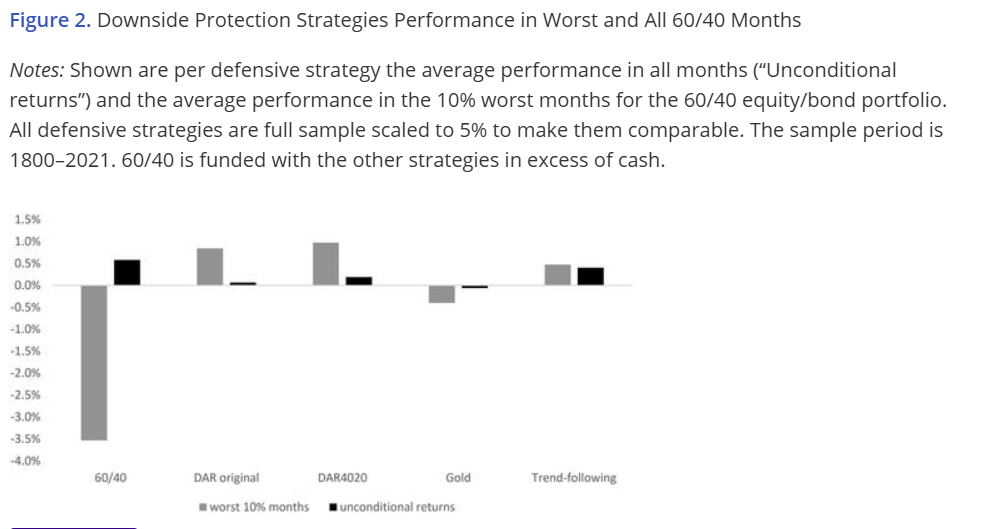

The main winners are trend-following and factor-following defensive overlays

During the worst 60/40 months, trend following and overlaying the protective factor called DAR (defensive absolute return) stand out as the most reliable help. In the worst 10% 60/40 months, trend following and the original DAR design both give positive average returns and they work more often than not. Traditional capital factors such as low risk, quality and value also help, but they tend to be weaker hedges than these two.

Gold looks like a hedge in recent history. In deep history there is none

Gold’s reputation as a safe haven is supported by several modern episodes, but the long sample does not support gold as a viable hedging strategy for 60/40 draws. In the authors’ tests, GOLD performs poorly in the worst 60/40 months over the full sample. This is a useful portfolio construction debugger that treats gold as a default hedge.

Install collision protection options, but tend to be expensive insurance

Equity index put overlays provide convex protection in sharp sell-offs, but the cost of long-term carry is significantly negative. The paper’s conclusion is consistent with previous work: systematic option buying is effective in the left tail, but tends to reduce long-term portfolio returns if not used selectively or explicitly funded.

A smarter DAR maintains protection and increases expected return

The original DAR portfolio was constructed by ranking a broad set of factor strategies by rotating the correlation to the 60/40 standard. It runs long in the most negatively correlated tercile and short in the most positively correlated tercile, producing a negative correlation but near-zero long-term return from construction.

The authors propose DAR4020: long 40% of the most negatively correlated factors and short 20% of the most positively correlated factors. This retains much of the hedge’s correlation profile while creating long net exposure to factor premiums. The result is a strategy that aims to provide protection with a more stable full-cycle return profile.

Trend tracking and DAR4020 are complementary and not substitutes

The paper documents a practical asymmetry. Trend following is often less useful at the start of pullbacks, especially when declines are sharp and short-lived, because signals can be slow to reposition at turning points. In contrast, the DAR4020 tends to provide immediate protection because it is structurally positioned with negative 60/40 beta. During longer pullbacks, trend following tends to “catch up” and often becomes very effective. A mixed split improves stability in all forms of traction.

Practical applications for investment advisors

Treat hedging as a portfolio design problem, not a product choice

The evidence supports the combination of protective sleeves rather than relying on a single protection. A balanced overlay of trend following and DAR4020 can reduce the depth of the pullback while maintaining a positive expected return profile, improving the likelihood that clients can maintain protection through extended bull markets.

Prioritize strategies with expected positive long-term returns

A defense that constantly loses money is difficult to sustain in practice, regardless of the theoretical benefits in the crisis months. The authors’ emphasis on hedging strategies with long-term positive returns is consistent with implementation reality: positive carry helps finance transaction costs and reduces the risk of abandoning the hedge before it is needed.

Stress test all regimes, not just the crises you remember

The deep sample includes periods with very different monetary systems, wars, trade shocks, and inflationary regimes. Defensive strategies that only work in the post-1985 world are fragile. Strategies that show resilience in radically different regimes are the ones you can discuss with a straight face in an Investment Policy Statement.

How to explain this to customers

“Most of the time, a balanced portfolio of stocks and bonds mixes well. The problem is that there are periods when it experiences deep pullbacks, and those pullbacks slow the accumulation of wealth. This research looks back roughly two centuries and finds that the most reliable hedges are not what people often assume. Gold is volatile, and buying put options all the time is usually very expensive. The strongest approaches are systematic trend following and a diversified hedge constructed from strategies that historically move differently than stocks and bonds. Because each helps in different types of selling, their combination tends to produce more consistent protection.”

The most important chart from the paper

Results are hypothetical results and are NOT an indication of future results and do NOT represent returns actually achieved by any investor. Indices are not managed and do not reflect management or trading fees, and one cannot invest directly in an index.

ABSTRACT

We examine hedging or hedging strategies over more than 220 years of global financial history, covering many years in which traditional bond-stock portfolios suffer and across a wide range of economic scenarios and historical regimes. Traditional equity hedging factors – low risk, quality and value – consistently provide effective downside protection, while gold and put options prove less attractive or cost-effective. Our long-term evidence shows that multi-asset hedge strategies, specifically a return-enhanced version of the hedge absolute return (DAR) portfolio introduced by Cavaglia et al. (2022) and trend following provide the most effective downside protection. DAR and trend following are complementary throughout tests diversifying each other in withdrawal phases. Investors can enhance the hedging properties and improve the total portfolio results of traditional portfolios by considering the in-depth sample evidence on the hedging strategies provided in this document.

–

Important discoveries

For informational and educational purposes only and should not be construed as specific investment, accounting, legal or tax advice. Some information is considered reliable, but its accuracy and completeness cannot be guaranteed. Third party information may become out of date or be replaced without notice. Neither the Securities and Exchange Commission (SEC) nor any other federal or state agency has approved, determined the accuracy, or confirmed the adequacy of this article.

The views and opinions expressed herein are those of the author and do not necessarily reflect the views of Alpha Architect, its affiliates, or its employees. Our full disclosures are available here. Definitions of common statistics used in our analysis are available here (in the last direction).

Join thousands of other readers and subscribe to our blog.