Stock momentum has long been a big idea. Shop the latest winners. Last losers for sale. Critics argue that those gains come largely from the trends of riding factors such as value, size or industry sentiment. This letter pushes back. It shows that there is a consistent stock-specific momentum component associated with how prices react to strong news around earnings dates. The result is a cleaner, lower-risk way to capture momentum without relying so heavily on broad factor movements.

The Many Facets of Stock Momentum: The Differentiating Factor and Components of Stocks

- Gerard and Jehl

- Financial Analyst Magazine, 2025

- A version of this paper can be found here here

- Want to read our summaries of academic finance papers? Check out our Academic Research Overview CATEGORY

Key academic insights

There is real momentum specific to stocks, not just factor timing

The authors isolate the portion of the 12-month momentum that comes only from returns in short windows around each firm’s earnings announcements over the past year. This component of the earnings announcement predicts future returns in the US, Europe and Japan over three decades. It remains significant after controlling for changing factor exposures.

Classic moment loads factors. the profit-advertisement component does not have

Traditional 12-1 momentum carries significant exposure to market, value and industry effects. of earnings-advertisement the strategy shows much lower systematic risk and a high correlation between long and short legs. This makes it a cleaner expression of firm-level information

Short-term PEAD has faded. The momentum of longer-term announcements continues

Strategies that trade only on the last earnings surprise have weakened in recent years. The collection of all notification windows over the past year continues to work. The turnover is also about half that of the short-horizon approach.

Factor momentum could mean classic momentum in US stocks. but not the announcement component

The principal component factor-momentum strategy is strong in the US and explains the classic momentum. It does not explain the long-term earnings announcement strategy. This part remains stable economically and statistically.

Long-term behavior changes. classic moment may change. the momentum of the announcement is not there

When you extend the formation to 24 months and skip a year before holding, the classic momentum shows reversals in the early 2000s, consistent with previous evidence of overreaction. The earnings announcement component shows no short- or long-term change, consistent with the low response to firm-specific news.

Practical applications for investment advisors

Separate the signal from the pier

When you use momentum, break it down. Keep the earnings announcement component as an essential sleeve. Treat the rest as more factor-oriented and size it accordingly.

Reduce unwanted bets

Industry-fix or defense-style anime if you have a classic vibe. Building the announcement-only newspaper naturally cuts market and value exposures. This can reduce drawdown risk when factor cycles roll.

Trade sensibly

The aggregated announcement signal for the year lowers turnover against short-term PEAD trades. Apply basic turnover control and realistic cost assumptions. The authors show that the premium survives reasonable friction in large, liquid names.

Use spaces and buffers

Skip the most recent month when using Classic Moment. The announcement strategy is less sensitive, but adding a small implementation delay and buffers helps reduce microstructure noise.

How to explain this to customers

“Momentum isn’t simply the direction of broad-based trends. Some of it comes from markets slowly disseminating company-specific earnings news. By focusing on those short announcement windows, we can isolate a more stable form of momentum with fewer hidden bets on value, size or industry effects. It’s a cleaner way to use momentum in a diversified portfolio.”

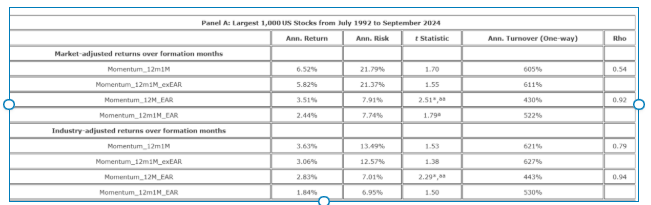

The most important chart from the paper

Table 2 shows a comparative analysis of the performance of a traditional stock momentum strategy and that of a long-term earnings announcement strategy in the large-cap segments of three developed markets: the US, Europe and Japan.

Results are hypothetical results and are NOT an indication of future results and do NOT represent returns actually achieved by any investor. Indices are not managed and do not reflect management or trading fees, and one cannot invest directly in an index.

ABSTRACT

This study aims to investigate the recent controversy surrounding the existence of specific stock momentum. Stock momentum consists of factor and stock-specific components, but the risk associated with factor momentum can offset the impact of stock-specific momentum. By using earnings announcement returns that occur during the formative months of the stock momentum strategy, the study captures a largely unaffected component of factor momentum, thereby mitigating the bad model problem. This stock-specific source of momentum predicts future returns, does not change over the long term, and is widespread, as similar results have been found in the US, Europe, and Japan over the past 30 years.

–

Important discoveries

For informational and educational purposes only and should not be construed as specific investment, accounting, legal or tax advice. Some information is considered reliable, but its accuracy and completeness cannot be guaranteed. Third party information may become out of date or be replaced without notice. Neither the Securities and Exchange Commission (SEC) nor any other federal or state agency has approved, determined the accuracy, or confirmed the adequacy of this article.

The views and opinions expressed herein are those of the author and do not necessarily reflect the views of Alpha Architect, its affiliates, or its employees. Our full disclosures are available here. Definitions of common statistics used in our analysis are available here (in the last direction).

Join thousands of other readers and subscribe to our blog.