For decades, when stocks dragged, bonds dragged, and the 60/40 investor slept like a baby. But over the past five years, bonds have begun to do something they haven’t done in decades: consistently correlate with stocks.. Worse, they have accompanied that new ascent with disappointing returns. Higher correlation, worse performance.

And with debt sustainability concerns looming on the horizon, many investors are now asking: are bonds worth holding? And if not, where do we go? true diversification?

Our friends at AQR took it upon themselves to answer both questions in their piece, A positive stock-bond correlation is a terrific reason to add more equity risk to your portfolio. In this post, I’ll walk through their findings, along with some numbers I’ve done myself, so you can think more clearly about what this means for your wallet.

Before we begin, if you prefer to watch the video version of this blog, be sure to subscribe to our YouTube channel and watch the latest episode on this topic.

Let’s begin.

Are bonds ever diversified?

Here’s the thing: In theory, if inflation is fully dampened by monetary policy, bonds should almost always be negatively correlated with stocks. But theory is not reality. And while bonds have certainly “got it” lately, I wondered how much of this experience is actually new.

So I ran the numbers.

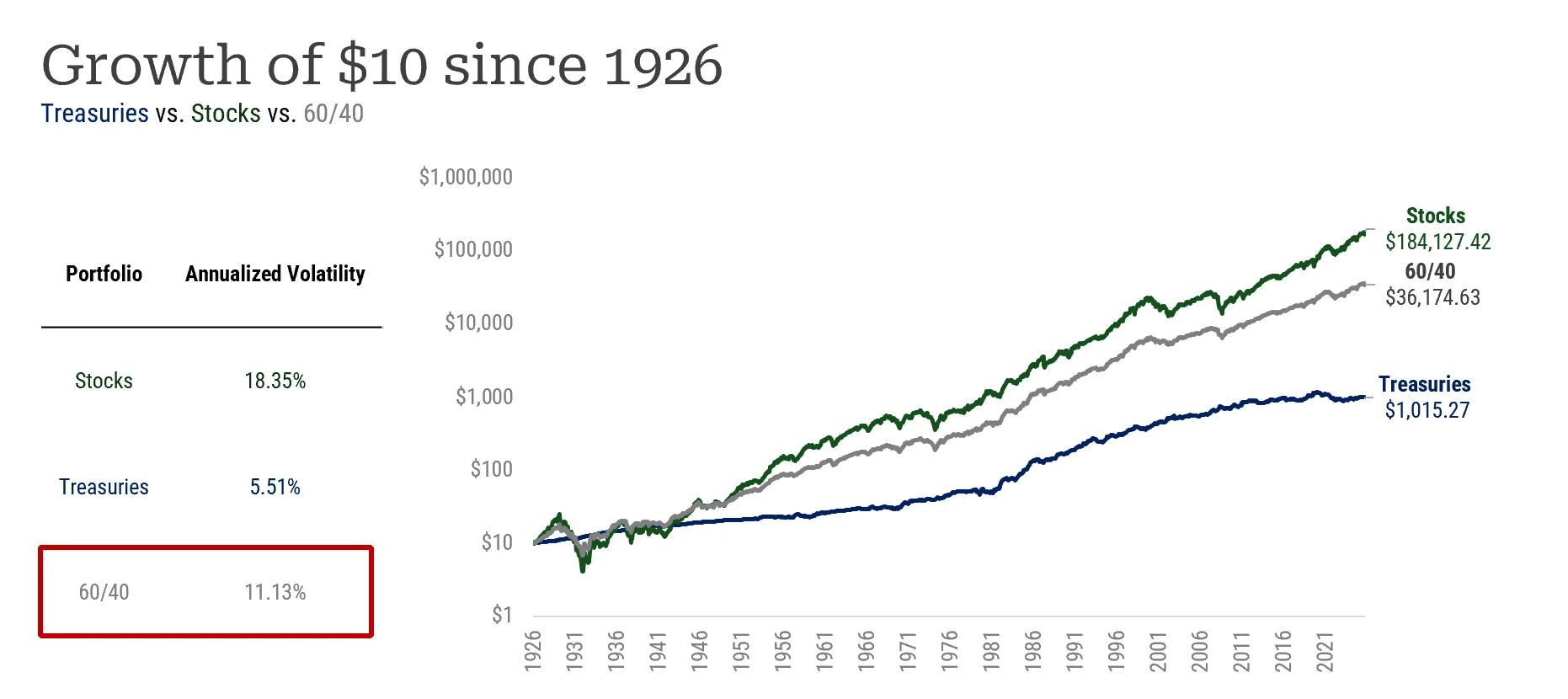

Thankfully, we have almost exactly 100 years of data from Kenneth’s French dataset to test how the classic 60/40 has done at the main job that investors hired him to do: diversification.

Historically, US stocks have yielded annual volatility of 18.35%, while bonds have yielded 5.51%. On the other hand, 60/40 had a realized volatility of 11.13%. But is this a good thing? A quick test we can do is to calculate the portfolio COMPLETED volatility and compare it with the ex-ante one weighted-average instability. If the realized volatility is significantly lower than a simple weighted average would predict, then we can conclude that the bonds did provide some level of diversification.

If you are curious, this weighted average is 13.22%. Do the math, and 60/40 has historically yielded roughly 16% less volatility than naive valuation would predict. Excellent! It appears that bonds have been a diversifying asset.

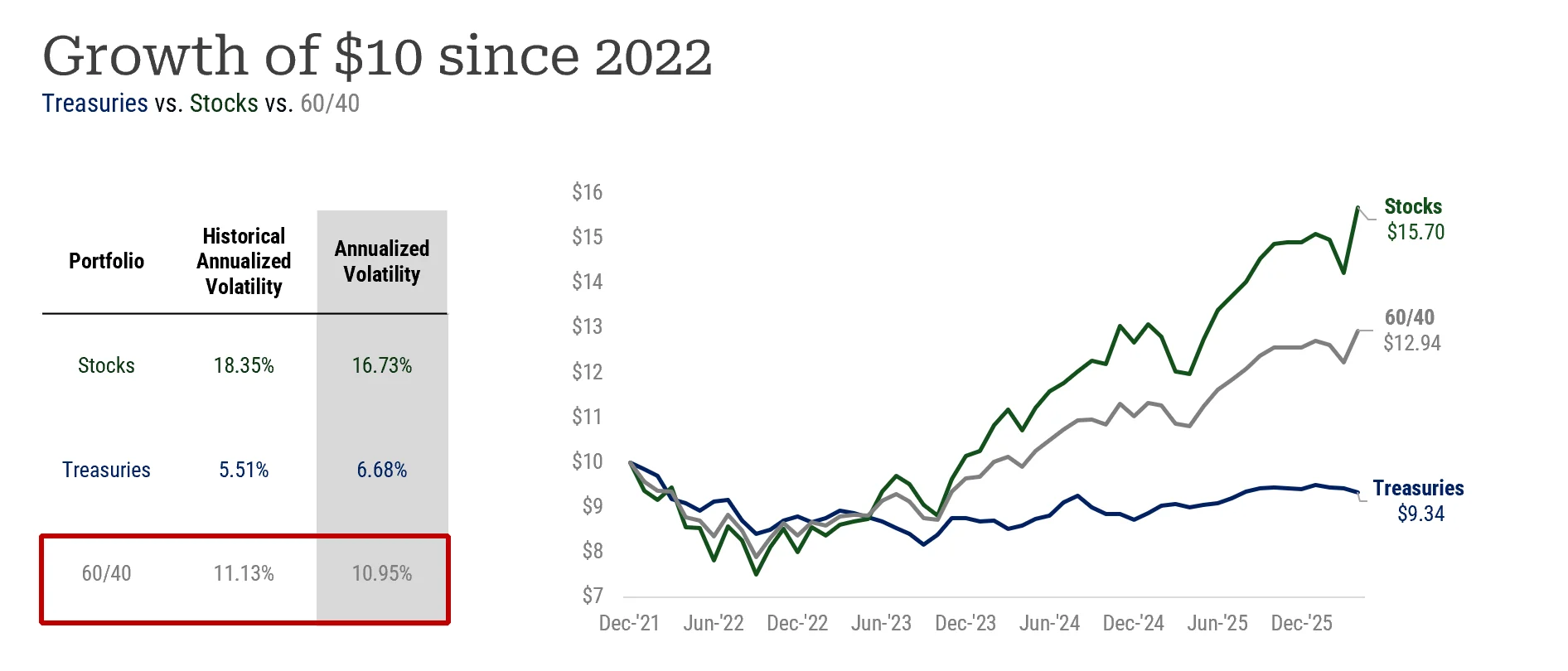

But what happens to the world after 2022?

Before you jump to the conclusion that those were just the “good old days” when bonds were used to diversify stocks, let’s crunch the numbers again, this time starting at one of the worst possible dates in three decades: 2022.

Since 2022, bond volatility has increased (6.68% vs. 5.51% historically) while stock volatility has actually gone DOWN (16.73% vs. 18.35%). And 60/40? A volatility of 10.95% which is… not that different from its historical reading of 11.13%.

Translation: yes, the benefits of diversification are more muted today. But they are not that different from their long-term average.

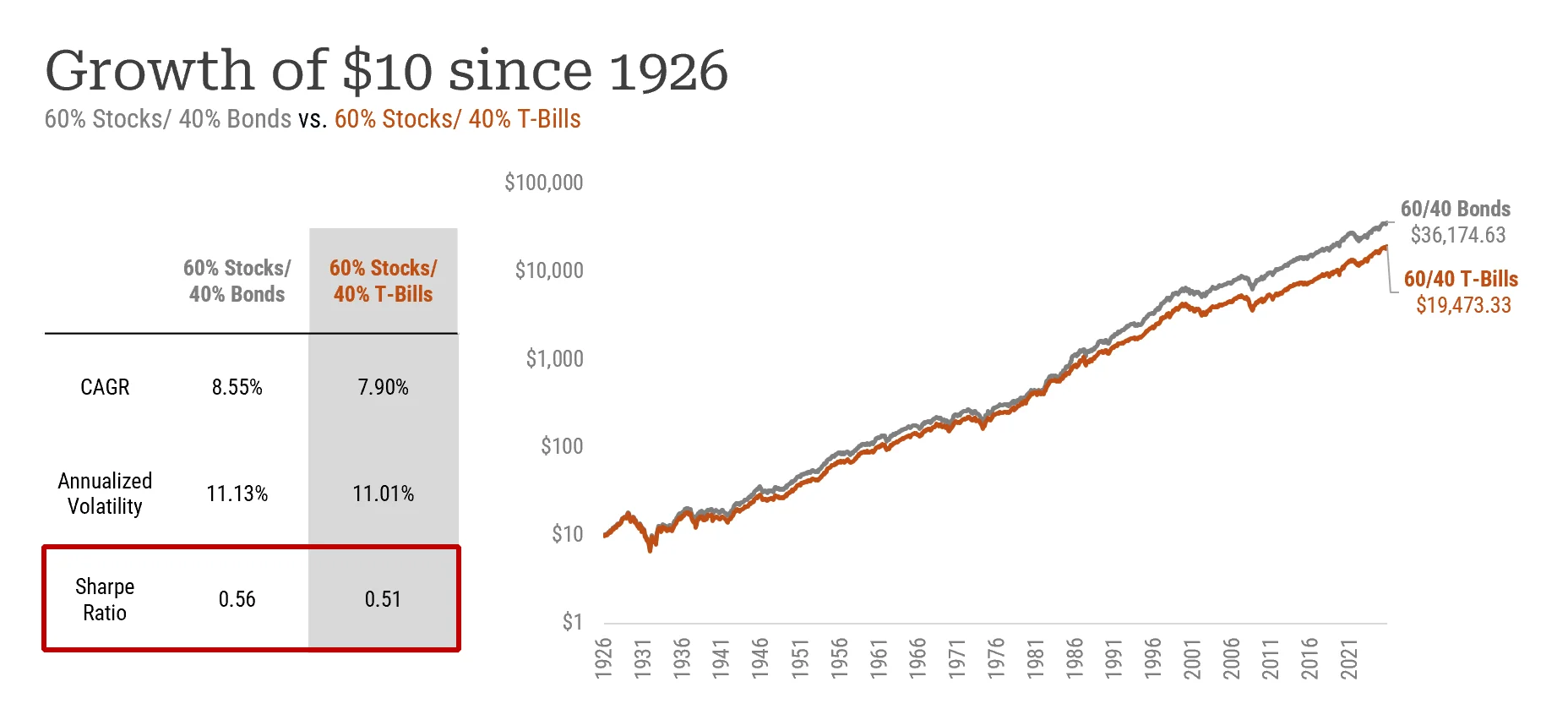

Portfolio 60% stocks/ 40% bonds

Okay, but surely a 60/40 in bonds is more than 40% in cash, right? Well: the bond version was built at approximately 8.55%, the cash version at 7.9%. Sharpe ratios? 0.56 versus 0.51. Bonds come out ahead, and while 65 basis points is compounded significantly over time, it’s not exactly a blanket result.

The main argument of the AQR team is that bonds dilute returns more than stocks diversify. Why? Because 60/40 returns are largely carried by equity sleeves. In fact, according to the piece, “in 49 of the last 50 years in which the S&P 500 lost money, a 60/40 US portfolio also lost money.”

There have been countless articles asking if 60/40 is dead. But they never ask if he was alive to begin with.

Popular (and delicious) substitutions.

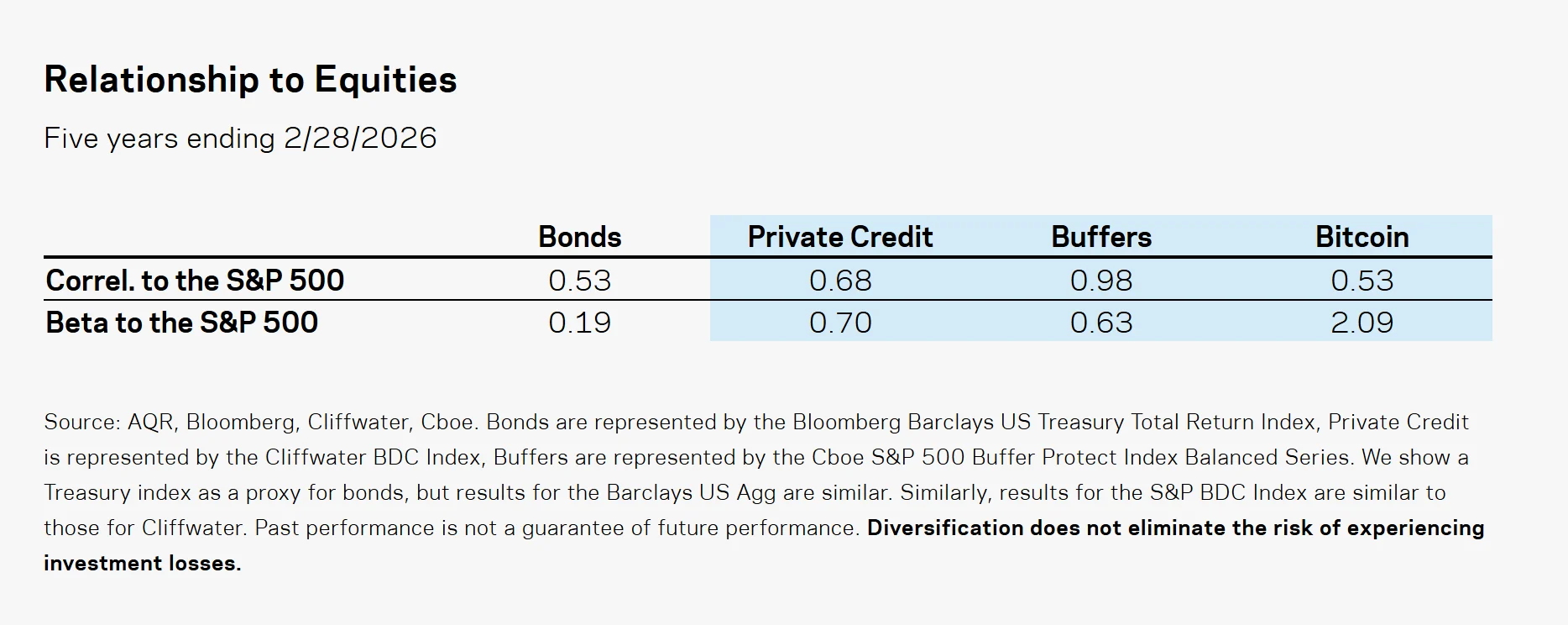

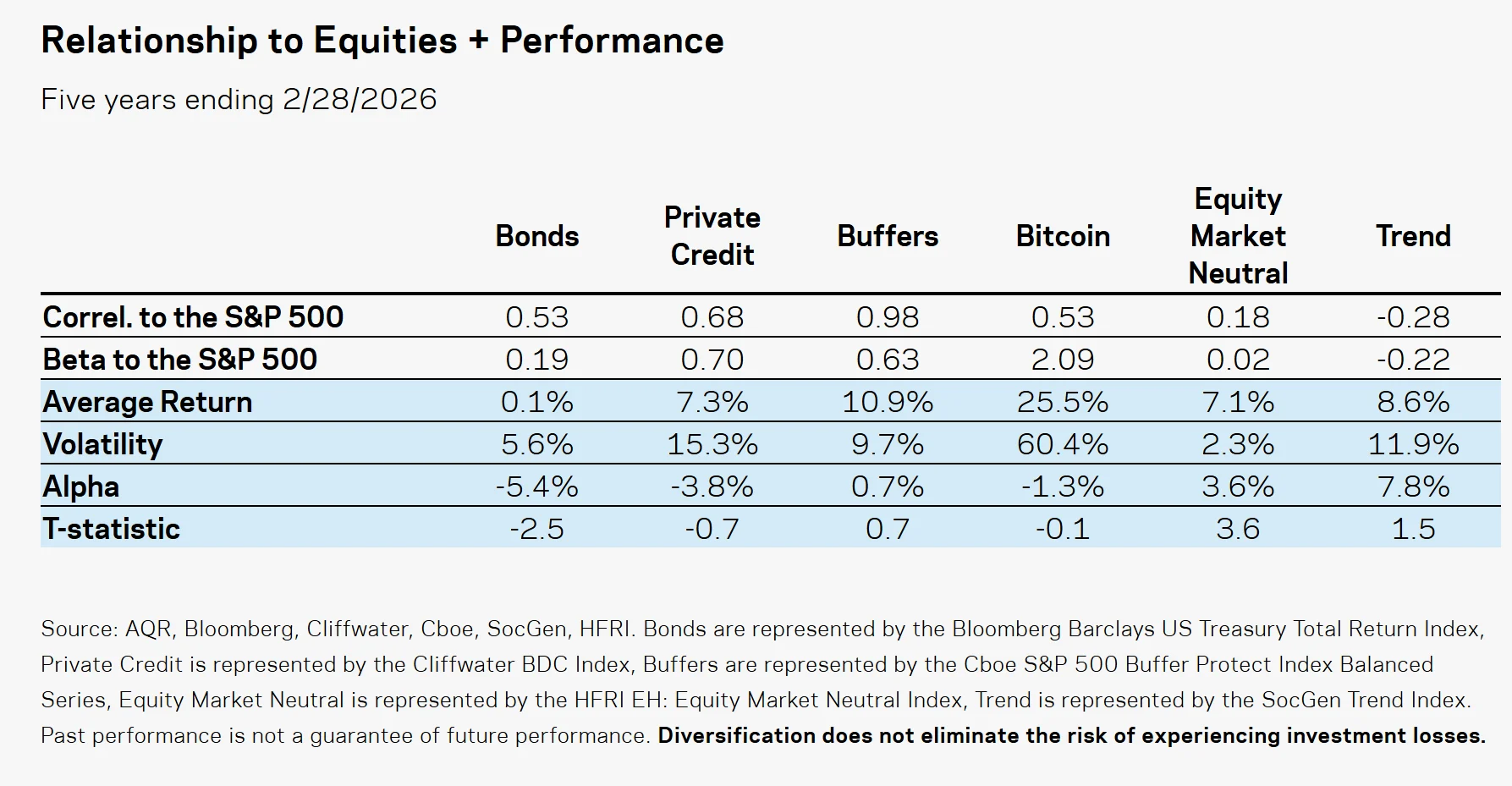

So investors are shopping for replacements. The paper examines three of today’s most popular candidates: private loans, buffer products, and yes, crypto.

The decision is not kind. Buffers have a 0.98 correlation with stocks—another sign that buffer returns can be largely recreated in stocks and cash. Private credit has a beta of 0.70. And bitcoin, the “least correlated” of the three, packs a beta of 2.09. After adjusting for those betas, both private credit and bitcoin have delivered negative alpha. You are getting worse results for the risk taken. Yes.

Where the real diversifiers live

The authors point to two top candidates:

- Neutral capital market. By going long stocks that are expected to beat the market and shorting those that are expected to lag, you can reap the factor premium at near-zero beta. This definitely stands out from the market.

- Trend following. By buying what’s going up and selling what’s going down, you can seek returns tied to macroeconomic disruptions.

Over the past five years, both have delivered what bond investors have been missing: correlations and betas close to zero or completely negative, with positive alphas early on.

So… Are Bonds Dead?

Now, I know it sounds like I wrote this post just to bust bonds. But (exactly) that’s not why I’m here. The lesson is not to run to sell your bonds. But if a positive stock-bond correlation makes you question your allocation, then apply a high diversification bar for everything you buy after that. You’d be surprised how the most popular alternatives fail that bar spectacularly.

Source: Asness, Cliff, Daniel Villalon, and Antti Ilmanen. “A positive stock-bond correlation is a terrific reason to add more equity risk to your portfolio.” AQR Capital Management, April 8, 2026.

Bonds don’t seem to diversify anymore. now what? originally published in Alpha Architect. Please read the Alpha Architect FINDINGS at your convenience.