For decades, long-term investing has been treated as a vague virtue rather than a distinct source of return. Markets are often assumed to be efficient over all horizons, with prices reflecting fundamentals, regardless of who holds the asset or for how long. Recent research challenges this assumption by showing that the very investment horizon of shareholders shapes future prices and returns.

Exploiting Myopia: The Return on Long-Term Investment

- Jain and Jiao

- Working paper, 2025

- A version of this paper can be found here here

- Want to read our summaries of academic finance papers? Check out our Academic Research Overview CATEGORY

Key academic insights

Investor myopia creates predictable mispricing

Professional investors face strong short-term performance pressure from defaults, buybacks and career concerns. As a result, they systematically avoid stocks that may underperform in the short term, even when long-term fundamentals are strong. This short-termism creates undervaluation that patient investors can exploit.

The ownership horizon matters at the firm level

The authors construct a firm-level measure of investor horizon based on how long active institutional investors currently hold a stock. Firms dominated by long-horizon owners earn significantly higher future returns than firms held primarily by short-horizon investors, even after controlling for standard risk factors.

Premium focuses where short-term constraints are most relevant

The long-horizon ownership return advantage is stronger among firms with high idiosyncratic volatility and low recent performance. These are the very stocks that short-term investors are least willing to hold due to temporary risk and career concerns.

The effect is driven by limitations, not superior abilities

Regulatory changes that increased short-term monitoring intensified the horizon effect, while improvements in information availability did not. This model shows that long-term investors earn excess returns not because they forecast better, but because they are willing to hold assets that others are forced to avoid.

Practical applications for investment advisors

The time horizon is a real investment constraint

Advisers must recognize that many investors, including institutions, are structurally unable to tolerate temporary underperformance. Strategies that require patience are not only psychologically difficult, they are institutionally out of reach for most of the market.

Discomfort is a signal, not a bug

Stocks avoided by short-term capital often seem unattractive precisely because they carry temporary volatility or trailing losses. For long-term portfolios, this concern may signal opportunity rather than risk.

Complement traditional factors with horizon awareness

Signals of value, profitability and quality tend to be stronger where investors’ horizons are longer. Understanding who owns a share, and how durable that ownership is, can improve the interpretation of traditional factor exposures.

Align portfolio construction with the true investment horizon

Long-term strategies require governance structures that tolerate tracking errors and temporary setbacks. Without this alignment, even theoretically sound strategies are likely to be abandoned at the wrong time.

How to explain this to customers

“Many investors are forced to focus on the next quarter, not the next decade. This short-term pressure takes prices away from long-term value. When you’re willing and able to underperform temporarily, you can earn returns that impatient investors leave behind.”

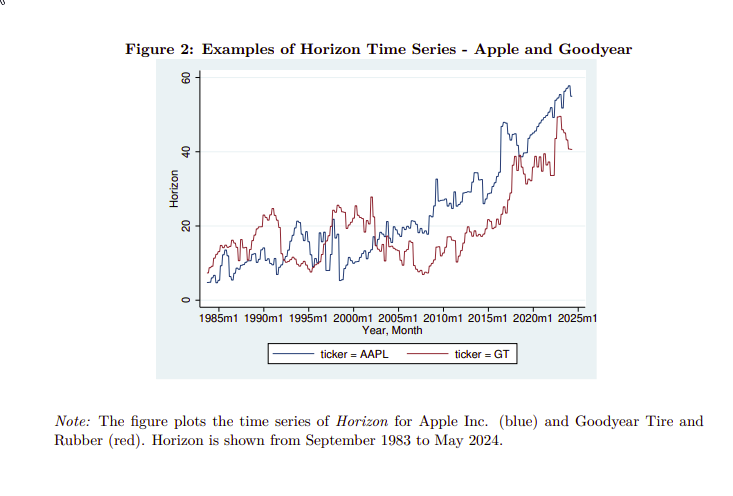

The most important chart from the paper

Figure 2 shows that the Horizon measure rises and falls around key firm-specific events that change who owns the stock and how long they are willing to hold it. For Apple, Horizon rose as the company matured and became a benchmark stock, while falling during leadership turmoil and market crashes. For Goodyear, activist battles, restructurings and crises caused sharp declines in Horizon, showing that the measure responds to real changes in investor behavior rather than hype.

Results are hypothetical results and are NOT an indication of future results and do NOT represent returns actually achieved by any investor. Indices are not managed and do not reflect management or trading fees, and one cannot invest directly in an index.

ABSTRACT

Investment managers often face short-term incentives, such as repurchase pressure after recent underperformance, that discourage them from holding positions through temporary underperformance. These limitations can lead to a systematic under-investment in firms that require longer holding periods to realize value. We examine whether these horizon-driven frictions generate predictable return patterns across firms. We measure long-term ownership at the firm level using active managers’ equity-weighted holding periods (Horizon) and document that firms with longer Horizons generate significantly higher returns than those with shorter Horizons, especially among stocks that are more difficult for myopic managers to hold. We use the 2004 SEC rule that increased the frequency of mutual fund disclosures to relate our findings to myopia. We find that treated firms experienced declines in the Horizon and a stronger Horizon return relation, consistent with increasing myopia, reducing the long run and increasing mispricing. In contrast, we find no change in the Horizon-return relationship after the XBRL mandate, which improved access to underlying information but did not affect investor constraints. These results suggest that frictions in institutional holding horizons, not information processing advantages, drive the observed returns to long-term investment.

–

Important discoveries

For informational and educational purposes only and should not be construed as specific investment, accounting, legal or tax advice. Some information is considered reliable, but its accuracy and completeness cannot be guaranteed. Third party information may become out of date or be replaced without notice. Neither the Securities and Exchange Commission (SEC) nor any other federal or state agency has approved, determined the accuracy, or confirmed the adequacy of this article.

The views and opinions expressed herein are those of the author and do not necessarily reflect the views of Alpha Architect, its affiliates, or its employees. Our full disclosures are available here. Definitions of common statistics used in our analysis are available here (in the last direction).

Join thousands of other readers and subscribe to our blog.