Mutual fund managers have long been thought to benefit from being close to the companies they follow. But what exactly creates that advantage? Better public information, faster internal communication or something more human? This paper argues that the missing piece is face-to-face contact itself. When the COVID lockdowns abruptly cut off in-person meetings, fund managers’ advantage in local stocks weakened, suggesting that part of the investment advantage still depends on trust, nuance and soft information that doesn’t travel so well across screens.

Face-to-face social interactions and the local information advantage

- Robin Y. Lee

- Journal of Financial Economics, 2026

- A version of this paper can be found here here

- Want to read our summaries of academic finance papers? Check out our Academic Research Overview CATEGORY

Key academic insights

Face-to-face contact seems to create a real local information advantage

Using the COVID-19 lockdowns as an exogenous shock, the paper shows that the performance of mutual fund managers in local stocks worsened relative to distant stocks when face-to-face meetings were restricted. The effect is not limited to weaker local economies. It appears at the worst time of investment in the same shares.

The economic effect is significant

After the lockdowns, benchmark-adjusted and DGTW-adjusted monthly returns in local portfolios were about 0.2 to 0.4 percentage points lower than in remote portfolios, compared to the period before the lockdown. For an average pre-lockdown local portfolio of $277 million, the paper estimates that a monthly drop of 0.4 percentage points means an annual loss of about $13.3 million per fund.

The mechanism looks like soft information, not just hard data

The author compares local and remote investors trading the same stock and finds that local funds increased portfolio weightings less aggressively following positive stock movements after face-to-face contact was discontinued. A one percentage point increase in a local position was associated with 1.3 to 1.5 percentage points lower abnormal return over the following three months, relative to remote positions, compared to the pre-lockdown period.

Building trust is one of the reasons why personal meetings matter

The paper argues that face-to-face meetings help build trust, which is important when information is soft, nuanced and difficult to verify. The negative effect of losing that channel is stronger when the trust distance between fund managers and corporate managers is higher. A one standard deviation increase in confidence distance is associated with a 0.79 percentage point lower forward period abnormal return for local investments versus distant investments, for a one percentage point increase in portfolio weight, after closures.

Impression management also matters, especially on the buying side

The deterioration is concentrated in buying rather than selling decisions, consistent with the idea that face-to-face meetings are particularly useful for conveying favorable soft information. The effect is also stronger for firms whose CEOs have higher pay-for-performance sensitivity, suggesting that executives with stronger incentives to shape investors’ perceptions benefit more from the face-to-face channel.

Practical applications for investment advisors

Be wary of assuming that all information travels equally well digitally

For local or relationship-driven investing, video calls and disclosures may not fully replace in-person access. If your process depends on management access, local networks, or private channel controls, treat the outage head-on as a real risk to information quality.

Pay more attention to less transparent names

The paper finds stronger effects in stocks with less transparent information environments, such as firms outside the S&P 500 and those with higher idiosyncratic uncertainty. This means that the local advantage may be more important in harder-to-read businesses than in big, heavily covered names.

Separate informational advantage from fundamental exposure

A useful due diligence solution is to ask whether a manager’s advantage comes from superior analysis of public data or from relationship-based access to soft information. These are different sets of skills and the second may be more vulnerable when travel, access or social contact is interrupted.

Do not confuse the lowest active part with the passive

The paper finds that managers reduced deviations from standard holdings after the lockdowns, but they still traded actively. This suggests that the problem was not a collapse in effort. It was a weaker signal environment. Counselors must distinguish between reduced persuasion and reduced ability to elicit information.

How to explain this to customers

“Being close to a company isn’t just about geography. It’s often about access. This paper shows that when face-to-face meetings suddenly disappeared, professional investors lost some of their edge in nearby stocks. In other words, some information is still better conveyed in person, especially when trust, nuance and judgment matter more than raw public data.”

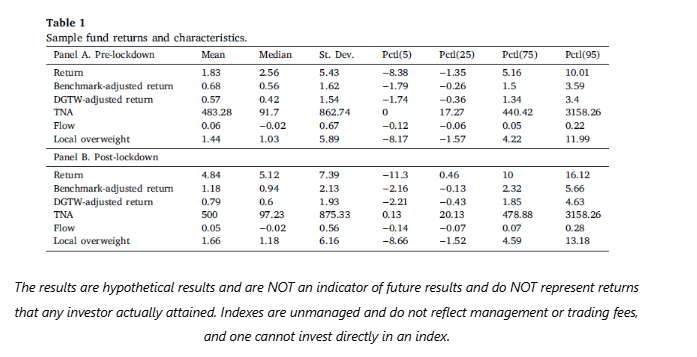

The most important chart from the paper

Table 1 summarizes the characteristics of the sample funds reported separately for the pre-block period (from January 2019 to the month before the implementation of the block orders at the fund location) in panel A and for the post-block period (from the month of implementation to December 2020) in panel B. Returns are calculated in monthly percentage points and reported. 𝑇𝑁𝐴 refers to the fund’s total net assets in millions. 𝐹𝑙𝑜𝑤 shows monthly fund inflows in decimal numbers.

𝐿𝑜𝑐𝑎𝑙 𝑜𝑣𝑒𝑟𝑤𝑒𝑖𝑔ℎ𝑡 is a measure from Coval and Moskowitz (2001) in percentage points.

Results are hypothetical results and are NOT an indication of future results and do NOT represent returns actually achieved by any investor. Indices are not managed and do not reflect management or trading fees, and one cannot invest directly in an index.

ABSTRACT

This paper examines the causal role of face-to-face (F2F) interactions in local information generation

advantages for mutual fund managers. Using the COVID-19 lockdowns as an exogenous shock, I show that the performance of fund managers in local stocks declined relative to distant stocks when face-to-face meetings were restricted, driven by investment timing impairment rather than changes in firm fundamentals. I investigate two distinct benefits of F2F interactions that arise from interpersonal cues: trust building, which enhances the transmission of soft information, and impression management, which facilitates the transmission of favorable information. The results cannot be fully explained by changes in internal information flows or the use of public information, and are more pronounced for stocks in less transparent information environments and in regions with stronger social characteristics.

–

Important discoveries

For informational and educational purposes only and should not be construed as specific investment, accounting, legal or tax advice. Some information is considered reliable, but its accuracy and completeness cannot be guaranteed. Third party information may become out of date or be replaced without notice. Neither the Securities and Exchange Commission (SEC) nor any other federal or state agency has approved, determined the accuracy, or confirmed the adequacy of this article.

The views and opinions expressed herein are those of the author and do not necessarily reflect the views of Alpha Architect, its affiliates, or its employees. Our full disclosures are available here. Definitions of common statistics used in our analysis are available here (towards the end).

Join thousands of other readers and subscribe to our blog.