Private equity has long been traded as the golden ticket. Higher returns. Exclusive access. Institutional level investments. The field is now simple. Bring it to retail portfolios, including 401(k)s. Critics argue that once you factor in fees, illiquidity and realistic fund selection, much of this advantage disappears. This paper pushes back the narrative. It shows that for most investors, private equity may not deliver the promised edge. And most importantly, it offers a simpler and more liquid way to access the same economic exposure.

- Nori Gerardo Lietz

- Harvard Working Paper Series, 2026

- A version of this paper can be found here here

- Want to read our summaries of academic finance papers? Check out our Academic Research Overview CATEGORY

Key academic insights

The high performance of private equity is less reliable than advertised

While PE funds have historically outperformed public markets in the top quarter, persistence has largely disappeared. Selecting future winners is extremely difficult. Most investors are likely to earn average returns rather than top-tier results.

Recent performance shows little or no alpha versus the public markets

When using more realistic methodologies that reconcile cash flows between the EP and the public STANDARDSexcess returns largely disappear. Over the past 15 years, private equity has delivered close to zero or even negative alpha relative to the S&P 500.

Fees materially erode returns, especially for retail investors

EP institutional returns are now free of significant fees. Retail access layers on additional costs from wealth managers, fund of funds structures and distribution channels. These additional fees can significantly reduce returns, often by double-digit percentages each year.

Fund of funds structures do not perform significantly

A common access route for retail investors is through brokers. Historically, these structures have consistently underperformed relative to direct PE investments and public markets, primarily due to fees and distribution inefficiencies.

Liquidity risk is real and often misunderstood

Private equity investments can lock up capital for 10-15 years. While some products promise periodic liquidity, redemption can disappear during market stress. Retail investors, unlike institutions, face real liquidity needs that make this limitation more problematic.

Industry dynamics suggest that future returns may be lower

The PE industry has grown dramatically, with trillions in assets and vast amounts of uninvested capital. High entry valuations and slower exits create headwinds for future returns, making historical performance less relevant in the future.

Publicly listed PE firms can offer a better one

A basket of publicly traded PE firms has historically outperformed their private equity peers over 5- and 10-year horizons. This approach provides similar economic exposure with lower costs and full liquidity

Practical applications for investment advisors

Focus on implementation, not just asset class tags

The question is not whether private equity is attractive in theory. It is whether customers can use it efficiently. In most cases, costs and implementation constraints dominate the outcome.

Be skeptical of “democratization” narratives.

Retail access often comes with additional layers of fees and complexity. What looks like inclusion may actually be the transfer of value from investors to intermediaries.

Prioritize liquidity as a key portfolio feature

Individual investors face unpredictable cash needs. Avoid locking up significant portions of portfolios in illiquid structures unless there is a clear and compelling return.

Consider the alternatives listed for exposure

Publicly traded PE firms provide exposure to the private markets economy without the operational burden. This can replicate many benefits while avoiding major drawbacks.

Control fees aggressively

Fees are compounded as are returns. An additional annual cost of 1–2% can wipe out most of the excess return expected from private equity.

How to explain this to customers

“Private equity is often presented as a way to earn higher returns, but the reality is more nuanced. Once you factor in fees, limited liquidity, and the difficulty of picking high-performing funds, the advantage becomes much less clear. In many cases, investors may be better off gaining exposure through simpler, more liquid public investments that capture similar economic benefits without adding up.”

The most important chart from the paper

The S&P returns generated over the same time periods are shown in Figure 1. The reported Horizon PE IRR returns have outperformed the S&P in each of the respective time increments. These are the figures that PE proponents have used to justify the distribution of PE capital. However, these comparisons are flawed in that IRRs and TWRs are calculated very differently, and the timing of cash flows has a material impact on IRR results. The Horizon IRRs above essentially “roll” each of the vintage years into a group and assume quarterly capital inflows and outflows. This is unrealistic considering that PE capital calls and

distributions occur throughout the year.

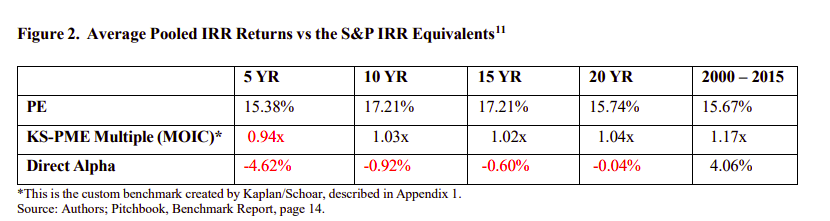

For Figure 2: Pitchbook undertook a more sophisticated analysis of PE versus public market performance. First, they created “pooled IRRs” by vintage year, which reflect the actual cash flows of all funds in the group as they occurred, as opposed to the simplistic assumption of treating all cash flows as if they occurred quarterly or annually. They then created a better comparison with the S&P by assuming analogous cash flows in the S&P that match those of the pooled IRRs.10 This analysis

generated a multiple return on invested capital (MOIC) at the end of the time period. In fact, Pitchbook created an IRR comparison with PE and S&P IRRs. Finally, Pitchbook then calculated the Direct Alpha (positive or negative) of the past year’s pooled IRR relative to the S&P. A score above 1 indicates high performance and a score below 1 indicates low performance relative to the S&P.

The annual performance results of each vintage for the past 23 years are shown in Exhibit 2. This methodology suggests very different conclusions than those in Figure 1.

Results are hypothetical results and are NOT an indication of future results and do NOT represent returns actually achieved by any investor. Indices are not managed and do not reflect management or trading fees, and one cannot invest directly in an index.

ABSTRACT

This paper examines whether private equity investments should be included in retail retirement portfolios such as 401Ks. While proponents argue that private equity offers higher returns and access to a wider investment universe, analysis challenges these claims. Evidence suggests that performance consistency has declined, excess returns relative to public markets have diminished, and additional layers of fees significantly reduce outcomes for retail investors. Given liquidity constraints and implementation challenges, the paper proposes an alternative approach: gaining exposure through publicly traded private equity firms, which can offer superior returns, lower costs and greater flexibility.

–

Important discoveries

For informational and educational purposes only and should not be construed as specific investment, accounting, legal or tax advice. Some information is considered reliable, but its accuracy and completeness cannot be guaranteed. Third party information may become out of date or be replaced without notice. Neither the Securities and Exchange Commission (SEC) nor any other federal or state agency has approved, determined the accuracy, or confirmed the adequacy of this article.

The views and opinions expressed herein are those of the author and do not necessarily reflect the views of Alpha Architect, its affiliates, or its employees. Our full disclosures are available here. Definitions of common statistics used in our analysis are available here (in the last direction).

Join thousands of other readers and subscribe to our blog.