Banks are supposed to have a unique advantage. Not only in lending. But in terms of borrowers, risk monitoring and intervention when things go wrong. For decades, theory has argued that this monitoring advantage is what makes banks special compared to nonbanks. However, direct evidence has been limited. This letter opens that black box. Using detailed, loan-level data and actual inspection reports, it shows how banks monitor borrowers in real time, how they act on that information, and how monitoring reduces the risk of default.

Bank Monitoring with On-Site Inspections

- Amanda Rae Heitz, Christopher Martin, Alexander Ufier

- Journal of Finance, 2026

- A version of this paper can be found here here

- Want to read our summaries of academic finance papers? Check out our Academic Research Overview CATEGORY

Key academic insights

Monitoring targets the riskiest borrowers and projects

Banks monitor more when the risk is higher. Loans with lower credit scores, higher loan-to-value ratios, speculative projects and inexperienced borrowers receive more frequent inspections. Monitoring is not random. It is actively distributed where the marginal benefit is highest.

Monitoring replaces stricter credit conditions

Loans with more intensive monitoring tend to have lower spreads and fees and larger loan sizes. This suggests a compromise. Instead of pricing risk entirely through higher interest rates, BANKS rely on monitoring to control risk dynamically over time.

Banks actively use real-time monitoring information

Inspection reports matter. Negative language in inspection reports is strongly associated with equalization denials, while positive language increases the likelihood of approval. This is direct evidence that banks process and act on soft information, not just hard metrics.

Monitoring responds to changing economic conditions

When local housing markets improve, banks monitor less and decline fewer withdrawal requests. When conditions worsen, especially with higher foreclosure rates, banks become tighter and deny more financing. Monitoring is adaptive, not static.

Monitoring reduces defaults, causally

Using an instrumental variables approach, the paper shows that increased monitoring significantly reduces loan defaults. The causal effect is great. Roughly speaking, a modest increase in inspection frequency can significantly decrease the probability of default, and standard regression methods actually underestimate this effect.

Practical applications for investment advisors

Monitoring is a major source of alpha in credit

This paper reinforces that credit investing is not just about selection. It is about constant supervision. Active monitoring can materially improve results, especially in uncertain or complex investments.

Dynamic risk management beats static underwriting

Risk cannot be fully assessed at origin. The ability to update views and act on new information over time is critical. Monitoring provides this flexibility.

Soft information matters

Quantitative models are not enough. Text, judgment and quality signals can drive real decisions. The fact that inspection language predicts funding decisions highlights the importance of qualitative analysis.

Incentives shape outcomes

The most powerful monitoring effect is often indirect. When borrowers know they are being watched, behavior improves. Structuring investments to create these incentives can be just as important as choosing the right opportunity

How to explain this to customers

“Banks don’t just lend money and wait to be repaid. They actively monitor borrowers throughout the life of a loan. This study shows that when banks closely follow how projects evolve and act on new information, they can significantly reduce losses. More importantly, the simple presence of monitoring encourages borrowers to behave more responsibly, before they fix problems.”

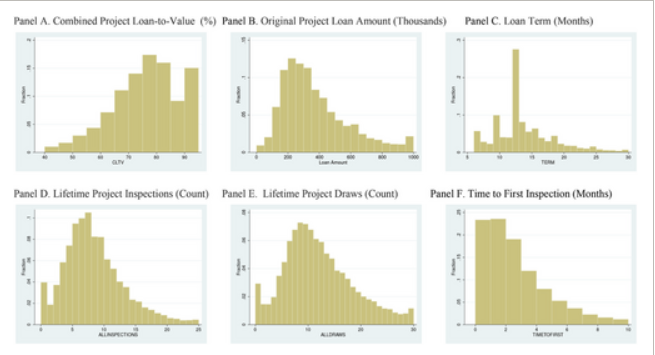

The most important chart from the paper

Figure 1 shows the relative frequencies for several loan level variables for the full sample of loans. Panels A and F report, respectively, combined loan to value (CLTV) of projects (reported as a percentage where 100 is 100% loan to value), original project loan amount in thousands, loan term to maturity in months, total lifetime inspections, total lifetime withdrawals, and time to first inspection per month.

Results are hypothetical results and are NOT an indication of future results and do NOT represent returns actually achieved by any investor. Indices are not managed and do not reflect management or trading fees, and one cannot invest directly in an index.

ABSTRACT

This paper provides direct empirical evidence on bank monitoring using proprietary data on nearly 30,000 construction loans and field inspection reports. The authors examine what drives monitoring decisions, how banks use information gathered through monitoring, and whether monitoring affects credit outcomes. They find that monitoring is more intensive for riskier borrowers and projects and is actively used in decision-making, with negative inspection reports leading to financing denials. The intensity of monitoring responds to changing economic conditions and increases as banks approach difficulties. Using an instrumental variable framework, the authors show that monitoring causally reduces loan defaults, with many benefits resulting from improved borrower behavior due to the threat of monitoring. Overall, the findings support theoretical models that emphasize monitoring as a key mechanism through which banks manage credit risk and improve lending outcomes.

–

Important discoveries

For informational and educational purposes only and should not be construed as specific investment, accounting, legal or tax advice. Some information is considered reliable, but its accuracy and completeness cannot be guaranteed. Third party information may become out of date or be replaced without notice. Neither the Securities and Exchange Commission (SEC) nor any other federal or state agency has approved, determined the accuracy, or confirmed the adequacy of this article.

The views and opinions expressed herein are those of the author and do not necessarily reflect the views of Alpha Architect, its affiliates, or its employees. Our full disclosures are available here. Definitions of common statistics used in our analysis are available here (towards the end).

Join thousands of other readers and subscribe to our blog.